Effective Bank Customer Retention Strategies

Banks have more customer data than almost any other industry, and still lose customers they could have kept. Here's how to match retention tactics to each stage of the banking life-cycle, and why customer feedback and personalisation only work when they're tied to the journey.

In this post, I examine the world of bank customer retention strategies, exploring how they can be optimised at different stages of the customer life-cycle. I take a closer look at two key tactics – leveraging customer feedback and personalisation – and examine how banks can implement these strategies effectively to keep their customers happy, engaged, and loyal long term.

So, whether you’re a banking executive looking to boost retention rates or a curious consumer wondering why your feedback seems to disappear into a black hole, read on to discover the secrets of successful customer retention in the banking industry.

Matching Customer Retention Strategies to the Customer Journey

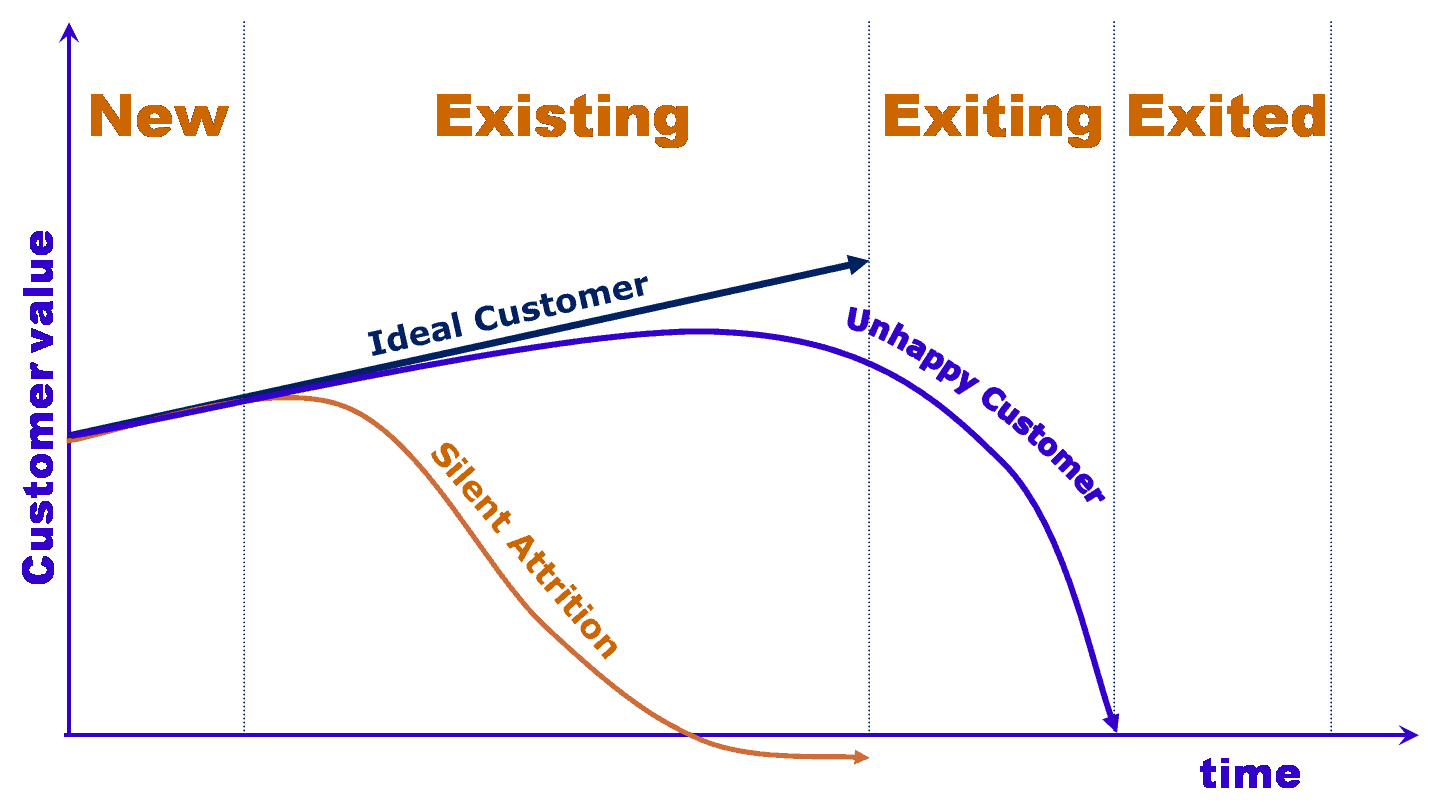

The banking customer journey is shown below, along with the value that different types of customers contribute to the business at different parts of the cycle.

New: Customers new to your organisation

The single largest group of customer retention strategies that can be implemented in the New section of the customer lifecycle is customer onboarding. Customer onboarding is the process of bedding a customer into your organisation and includes ensuring that their personal data is correct, that they understand the products they have purchased and how to quickly contact the organisation.

We have proved time and again that customers that are properly onboarded have a higher customer retention rate and spend more money than similar customers who were not onboarded.

Other areas of New customer management include:

- Data integrity management

- Cross-sell leads management

- Product benefit education

- Product activation

- Payment automation optimisation

Existing: Customers you already have

The best bank customer retention strategy for existing customers is to classify each type of customer (silent attrition, ideal and unhappy) and create appropriate initiatives to change their behaviour.

Customers in “silent attrition” are those that have reduced or stopped using a product, but the account is still open. For example credit cards linked to a checking account with little or no spending.

For these customers, you must determine why they are no longer using your product (are you are their “back of wallet” card) and create initiatives to change their behaviour.

Examples of Existing customer management programs include:

- Product design evolution

- Payment automation optimisation

- Active customer complaints management

- Cross-sell leads management

- Product activation

- Usage stimulation

- Preapproved products

- IVR Messaging Offers

- Leveraging sponsorships

- Leveraging affinity marketing

- High value relationship programs

- Low value relationship programs

- Local area marketing

- 3rd Party and Sales consultant commissions

- Driving customers to highest ROI channel mix

- Product bundling

- Product Upsell

- Silent attrition management

- Collections process

- Move and Follow

- Differentiated levels of service

- Optimising product mix

Exiting: Customer thinking of leaving

Customers that are Exiting are those customers that have started the process of moving their business to another company or are in the process of considering that move. The first step in creating bank customer retention strategies for Exiting customers is to identify which customers are in each camp.

For customers in the process of moving their business you will need to understand the product drop cycle, i.e. the order in which customers drop your products before leaving. With this information you can create effective customer retention strategies to target those customers.

One of the key programs that can be implemented in this phase is Save Teams.

Exited: Customers who have left

Generically, strategies that are aimed at recapturing customers that have left the organisation are called Winback strategies. This is the most expensive and lowest ROI place to try to implement your bank customer retention strategies. Mentally, customers have already moved to another organisation and it takes a large inducement to bring them back.

If you do choose execute Customer Winback strategies, then you will need to carefully manage the level of incentive that your staff can offer to customers. For instance, you will need rules to tailor the incentive level to each specific customer in order to ensure that the level of inducement is not larger than the future business generated by that customer.

Leveraging Customer Feedback for Retention

One of the most powerful tools for driving customer retention in banking is actively seeking and utilising customer feedback. Regularly conducting customer satisfaction surveys allows banks to gain valuable insights into the needs, preferences, and pain points of their customers at various stages of the life-cycle.

By asking the right questions and analysing survey responses, banks can:

- Identify areas of strength and weakness in their products, services, and overall customer experience.

- Uncover specific issues or friction points that may lead to customer churn if left unaddressed.

- Gauge customer loyalty and likelihood to recommend the bank to others.

- Segment customers based on their feedback and tailor retention strategies accordingly.

Armed with this information, banks can prioritise improvements and initiatives that directly address customer concerns and drive retention efforts. For instance, if surveys reveal dissatisfaction with digital banking platforms, banks can invest in upgrading their technology and user experience. If customers express a desire for more personalised financial advice, banks can develop targeted educational resources or enhance their customer support training.

Moreover, actively closing the loop with customers who provide feedback demonstrates that their opinions are valued and acted upon. This not only helps resolve individual issues but also fosters a sense of trust and loyalty that can prevent churn in the long run.

To maximise the impact of customer feedback, banks should:

- Implement a regular cadence of surveys across various touchpoints (e.g., post-transaction, annual relationship surveys)

- Use a mix of quantitative and qualitative questions to gather both measurable data and rich, open-ended insights

- Leverage survey tools and platforms that enable easy analysis and reporting

- Share feedback insights across the organisation and use them to inform retention strategies and initiatives

- Close the loop with customers and communicate actions taken based on their feedback

Using Personalisation Across the Customer Journey

Delivering personalised experiences and engagement throughout the customer life-cycle is crucial for driving retention and loyalty. Customers increasingly expect their banks to understand their unique needs, preferences, and financial goals, and to tailor their products, services, and communications accordingly.

To achieve this level of personalisation, banks must collect and use customer data from various touchpoints and interactions, banks can gain a comprehensive understanding of each customer’s behaviour, interests, and pain points.

This includes data from:

- Transactional history

- Product usage and preferences

- Customer service interactions

- Digital banking activity

- Demographic and life-stage information

Armed with these insights, banks can segment their customers and develop targeted retention strategies for each stage of the customer journey.

I’ve already outlined strategies for various stages of the customer journey and this information can be used to create more effective campaigns using those strategies.

But it can also be used to empower front-line staff with customer insights and training to deliver personalised service and advice.

Of course the use of customer information in this way must be done in line with data privacy and security as a key requirement.